# 1: Coronavirus Emergency Loans Small Business Guide and Checklist

For those looking for information regarding the CARES Act and how it affects small businesses, the U.S. Chamber of Commerce has released a useful Coronavirus Emergency Loans Small Business Guide and Checklist. Find it by clicking here.

You may also visit the U.S. Government Small Business Association's COVID-19 Resource and Loan Guide by clicking here.

# 2: Coping with Market Volatility: Avoid Rash Decisions

If you've been watching the market lately, perhaps the first question on your mind is, "Should I make a big change in my investments?" In reality, a volatile market isn't the best time to do a complete makeover of your portfolio, especially if you have long-term financial goals you're trying to address.

Even if you feel that your portfolio needs adjusting, maintaining a firm grasp on your fundamental investment strategy can help you be more thoughtful about making any changes.f you've been watching the market lately, perhaps the first question on your mind is, "Should I make a big change in my investments?"

In reality, a volatile market isn't the best time to do a complete makeover of your portfolio, especially if you have long-term financial goals you're trying to address. Even if you feel that your portfolio needs adjusting, maintaining a firm grasp on your fundamental investment strategy can help you be more thoughtful about making any changes.

Think of each investment as a tool in your investing tool kit, and your asset allocation strategy as your blueprint. Some investments are generally designed to pursue long-term growth, others to provide income, and still others to represent stability. Each is valuable in its own way, but it doesn't make sense to use a hammer to remake your portfolio if what you really need is a screwdriver to make minor adjustments.

Don't randomly abandon one investment for another unless you know its intended role in your portfolio, whether that role is still appropriate, and the pros and cons of any replacement you're considering.

Remember that diversification can help offset the risks of certain holdings with those of others. When one type of investment is losing ground, another may be gaining or holding steady.

Diversification and asset allocation cannot ensure a profit or guarantee against a loss, but they can help you understand and manage investment risk.

In these uncertain times, it's easy to let fear guide your decision making. But when it comes to your investments, a more rational outlook may be your strongest ally. We're here to help and to answer questions.

Although there is no assurance that working with a financial professional will improve investment results, a professional can evaluate your objectives and available resources and help you consider appropriate long-term financial strategies.

All investing involves risk, including the possible loss of principal, and there is no guarantee that any investment strategy will be successful.

Dorothy Austgen, CFP®, Karen Candiano, CFP®,

Niko Yates, Financial Advisor, Michael Gard, Financial Advisor

Securities offered through Lion Street Financial, LLC. (LSF), member FINRA & SIPC. Investment Advisory Services offered through Csenge Advisory Group, LLC. (CAG), Registered Investment Advisor. Additional Investment Advisory Services offered through Eley-Graham-Austgen Financial Advisory Services, not affiliated with LSF or CAG. LSF, CAG and Eley-Graham-Austgen Financial Advisory Services do not provide legal or tax advice. Representatives may transact business, which includes offering products and services and/or responding to inquiries, only in state(s) in which they are properly registered and/or licensed.

IMPORTANT DISCLOSURES Broadridge Investor Communication Solutions, Inc. does not provide investment, tax, legal, or retirement advice or recommendations. The information presented here is not specific to any individual's personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable — we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

This communication is strictly intended for individuals residing in the state(s) of AL, AK, AZ, AR, CA, CO, CT, FL, GA, IL, IN, IA, KS, KY, MI, MN, MS, MO, NC, OH, PA, SC, SD, TN, TX, VA and WI. No offers may be made or accepted from any resident outside the specific states referenced.

Prepared by Broadridge Advisor Solutions Copyright 2021.

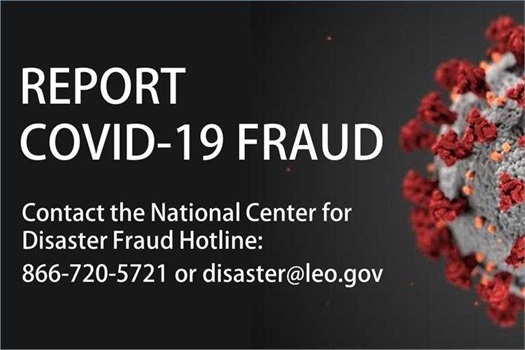

#3 Covid-19 Fraud Alert

From the United States Department of Justice: "Be aware that criminals are attempting to exploit COVID-19 worldwide through a variety of scams.

There have been reports of:

• Individuals and businesses selling fake cures for COVID-19 online and engaging in other forms of fraud.

• Phishing emails from entities posing as the World Health Organization or the Centers for Disease Control and Prevention.

• Malicious websites and apps that appear to share virus-related information to gain and lock access to your devices until payment is received.

• Seeking donations fraudulently for illegitimate or non-existent charitable organizations."

For more information, visit the USDJ here or go to https://www.justice.gov/coronavirus

------

| |||||||||||||||||||||

#4: Coronavirus and Retirees

As you probably know, Congress passed the largest stimulus package in American history, the Coronavirus Aid, Relief, and Economic Security Act (CARES). This was done in an effort to combat some of the pandemic’s harmful economic effects. And while many American investors are feeling financially overwhelmed, retirees may be in an even trickier situation.

Not only are you caught in this economic crunch, but you’re doubly burdened by the greater health threat this virus may have on older people. Because of that, Congress passed portions of the CARES Act to positively impact the health and well-being of retirees, as well as provisions that benefit those still significantly invested in the markets.

Here are the portions of the stimulus bill that will likely have an impact on financial decisions you’ll be facing in the near future:

Stimulus check. One of the most talked about benefits of the stimulus package is the $1,200 stimulus payments for individuals who earned $75,000/year or less and $2,400 for married couples filing jointly that earned $150,000/year or less. This also includes seniors who don’t normally owe taxes and those claiming social security benefits, including retirement and disability. If you don’t need the extra money to make ends meet right now, consider tucking this check away in an emergency fund.

IRS tax deadline extension. The IRS is extending the federal income tax filing due date of April 15 to July 15, 2020 instead, without penalty or interest. This is an automatic extension that applies to all taxpayers, regardless of the amount owed, including individuals, trusts and estates, and those who pay self-employment tax.

IRA contribution extension. Along with the tax filing extension of July 15, 2020, comes an extended deadline for contributing to last year’s IRA. If you get a stimulus check and haven’t yet reached the $6,000 max (or $7,000 if you’re older than 50) for 2019, consider adding it there.

Required minimum distribution (RMD) suspended for 2020. Retirees will not be required to withdraw any amount from their retirement accounts, and no penalties will be assessed.

Nursing home and senior living attention and funding. Both the Centers for Medicare and Medicaid Services will get additional funding with the intention of providing safer, cleaner facilities to prevent the spread of the coronavirus.

Enhancements to Medicare and Medicaid services. There are numerous ways in which this law will assist in getting health services to retirees more quickly, including “telehealth" coverage, 90-day prescription refills and the extension of existing community-based, long-term care programs.

Many of these changes provide extra funding for unavoidable hardships, given the state of the economy and the state of global health. If you have any specific questions on how the coronavirus crisis will impact your retirement, let’s talk. As always, we’re here to help.

#5 Frequently Asked Questions about 2020 Stimulus Checks

FAQs About the 2020 Stimulus Checks

Answers to some frequently asked questions.

Provided by Eley-Graham-Austgen Financial Advisory Services

The federal government is providing a little economic relief to many taxpayers. The Internal Revenue Service is sending millions of Economic Impact Payments – or as they are commonly called, stimulus checks – to households.

Here are some facts to know about these payments. Keep in mind: this article is for informational purposes only. It’s not a replacement for real-life advice, so make sure to consult your tax professional before modifying your strategy.

Who gets a check? If you have a Social Security Number and have not been claimed as a dependent on another taxpayer’s most recent federal tax return, you may be eligible for a stimulus payment of up to $1,200. Any money you get is tax free, and the payment will not be counted against a federal tax refund coming your way or federal benefits you currently receive.1

Can I get a direct deposit rather than a paper check? Yes, assuming you provided a bank account number to the I.R.S. when you last filed federal taxes. If you did, the I.R.S. can route the stimulus payment right into that bank account. Another option is to update your account information through the I.R.S. website. Absent of such information, the I.R.S. will mail you a check instead.1

When will my payment arrive? Secretary of the Treasury Steven Mnuchin expects that most eligible taxpayers will receive their stimulus money in April. Taxpayers waiting for a check in the mail may get their payments later.2

Where can I track my payment? Visit irs.gov/coronavirus/get-my-payment to check its status.3

Will most eligible taxpayers receive the full $1,200 payment? Yes. The payment amount is calculated using your adjusted gross income (AGI) from your most recently filed federal tax return. A qualifying single filer with AGI of $75,000 or less will get the full $1,200. The same goes for someone filing as a head of household who has an AGI of $112,500 or less.2,4

Joint filers (i.e., married couples) with an AGI of $150,000 or less will get a total of $2,400. Joint filers and heads of households who have kids may get more – specifically, an additional $500 for every qualifying child younger than 17. (A married couple or head of household with three young children could receive nearly $4,000.)2,4

Single filers with AGIs of more than $99,000, child-free heads of household with AGIs of more than $136,500, and child-free joint filers with AGIs above $198,000 will not receive stimulus checks.2,4

Single filers with gross incomes of $12,200 or less in 2019 and joint filers with gross incomes of $24,400 or less in 2019 must visit irs.gov/coronavirus/non-filers-enter-payment-info-here to facilitate their payments. This also applies to taxpayers who have not yet filed a 1040 form for the 2019 tax year or have no plans to do so.2,5

Do you have to repay the money later? No. The stimulus payment is not a loan to you from the federal government. Misinformation about this is circulating, and as MarketWatch notes, it may stem from the way the stimulus checks are technically defined. Technically speaking, the stimulus money is a 2020 federal tax credit. The I.R.S. is effectively giving an advance tax refund to eligible taxpayers. One asterisk, though: if you owe child support, the I.R.S. has the option to use some or all of your stimulus payment to reduce the outstanding amount.6

Does this stimulus payment count against your 2020 taxes? No. It impacts neither federal tax refunds nor federal tax liabilities.6

Questions? Call us at 219-736-6900.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note - investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

Citations.

- BusinessInsider.com, April 22, 2020

- The New York Times, April 16, 2020

- IRS.gov, April 21, 2020

- TheBalance.com, April 10, 2020

- IRS.gov, April 22, 2020

- MarketWatch.com, April 18, 2020